Quiet Contrarian. Ep4: Lessons from Losses

Continuing on my review of past performance, I wanted to revisit a few of my winners and losers, and the key lessons I learned from them. This week I’ll start with my losses.

Sunbridge Group Limited (SBB:ASX) – Sunbridge was a clothing retailer from China. By the books they were incredibly undervalued (from memory, I had their valuation at about $1, and they were trading at ~20c). This seemed to be too good to be true! I felt like they were a diamond in the rough, here was this amazing company that no one else knew about. So I bought in. Then the price crashed to 8c. I was surprised, but stuck to my initial guns, and tripled my investment in the company. Fortune favours the bold! I held them for the next 2 years, before finally getting out at 2c per share. In the end I’d lost 88% of my initial investment.

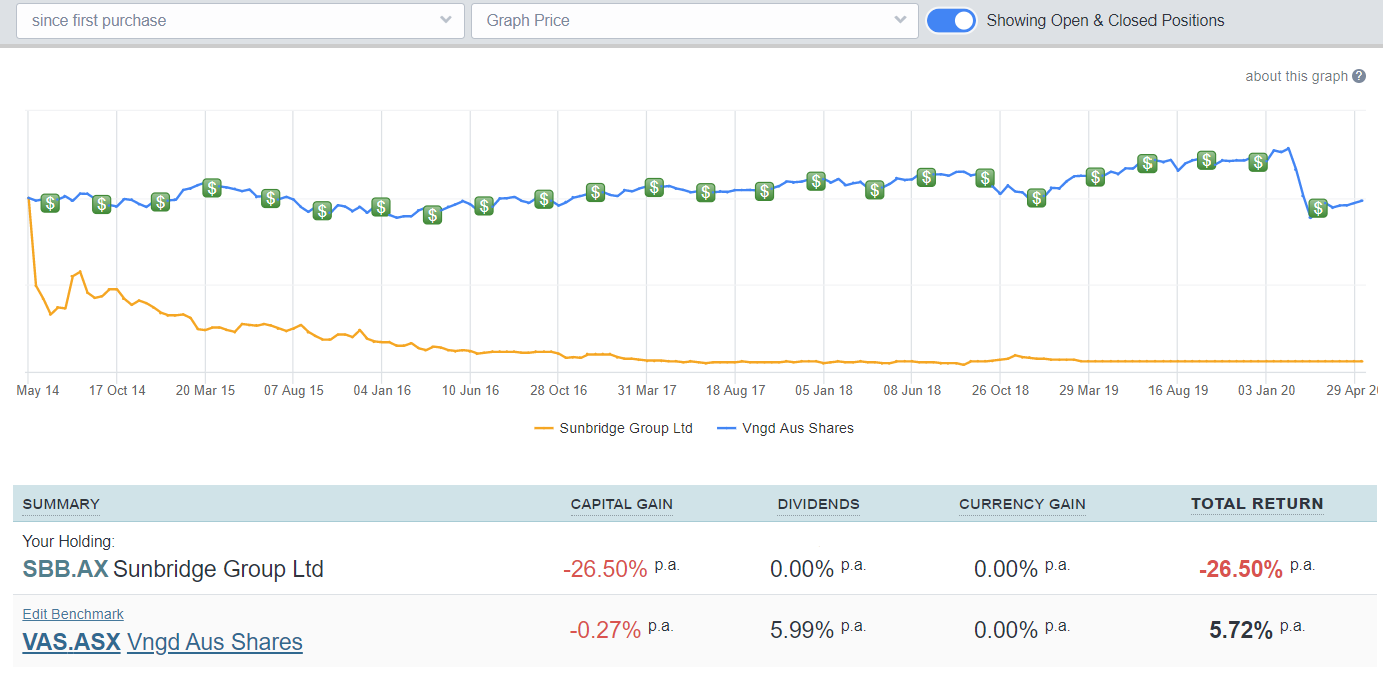

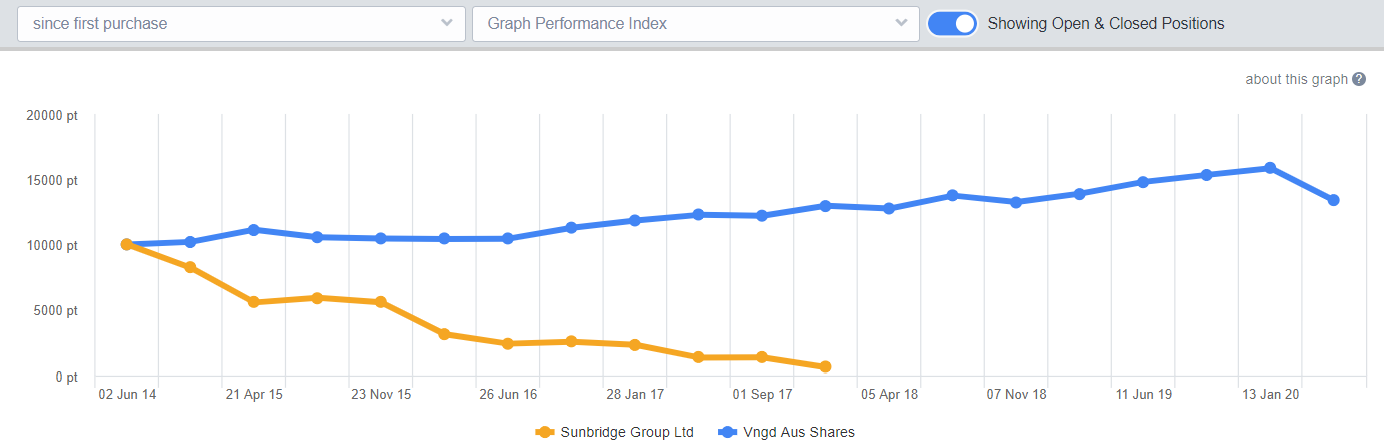

This is what the stock price of SBB looked like relative to the Australian Market.

This is what the performance of my investment looked like.

In hindsight, I really didn’t know anything about the company, I’d been blinded by the numbers of what seemed like an amazing deal without knowing enough about the business. I didn’t know what to look for in financial reports (I’m not sure I even looked at the financials). I didn’t know how to read the signs in the market. At one point I remember reading that they had enough cash on hand to pay 6c to every shareholder if they dissolved the company. But the company was trading at 1-2c per share at this point. No one believed that money was ever going to get back to the shareholders, and they were right.

Lessons Learned:

- The numbers aren’t everything, if it looks too good to be true, it probably is.

- Companies don’t have to act in the best interests of their shareholders, trustworthy management is worth it’s weight in gold.

Beyond International (BYI:ASX) – I still have a soft spot for this company. It was one of my first purchases, and they aren’t a bad business, they’re well run, their books are managed well, but their profit got hit hard in recent years. They were in the wrong part of the industry and failed to see the writing on the wall and pivot their business model to get ahead of the game (think Blockbuster vs Netflix).

Why did I buy?

In 2013 BYI looked amazing, they were highly profitable, their TV production segment and their home entertainment segments were doing great.

What went wrong?

I failed to understand the nitty gritty of their business model. Including what was making them money, and how those industries would change over the next few years. Two big things changed as far as I can tell:

- BYI don’t release the details of how individual shows contribute to their earnings, but amidst all their myriad of reality TV productions, they had one show I’d heard of, Mythbusters. I suspect this was their major success story and drove a lot of their earnings. In 2014, this was reaching the tail end of interest, and none of the spinoffs seemed able to recapture the former glory.

- The second part of the failing business was Home Entertainment. They sold physical media, y’know, things on discs. This market has been shrinking every year for the last 5, and they’re still selling them. The market isn’t going to turn around. No one is going to give up streaming media for a return to buying things on disc. This stream is just bleeding out, the earnings from it go down every year, and I don’t think it’ll come back.

What was holding them like?

When the price first fell, I remember thinking, “oh that was a bad year, Mythbusters isn’t doing as well, but they’ll have another hit. It can’t get any worse”. Then the next year the DVD division started failing, and they announced a streaming media division “Oh that was bad, but the DVD sales has reached bottom, and this new revenue stream will make up the cash”. The year after that, plummeting DVD sales saw a renegotiation of all the sales contracts which resulted in still lower profit margins. “Oh that was bad, but it can’t get any worse…” and so on it went.

I liked the company (and still do), but kept waiting for a turnaround that never came. This is what a slow bleed out looks like. Over the ~5 years I held onto them, I got 12% of my initial investment back in dividends, and lost 27% of my initial money. I didn’t get out at the worst point, so in that respect my patience paid off, but I would have been better off if I’d gotten out sooner.

In hindsight, I should have paid more attention to the market trends and been more honest about their prospects. I let my biases colour my view and only saw the rosy picture. After a few years, it was obvious that the DVD market was bleeding out and that this was going to continually drag down their profits. I was blinded to the numbers of this, by their production division. “If they just find a new hit…” but this is a bit of a lottery. The fact that I’d never heard of the hundreds of shows they’d produced should have spoken far more volumes than the one show I did watch. The likelihood of this was far lower than it seemed. The fact of the matter was I didn’t look at the bigger picture and the actual business performance. I’d latched onto all the reasons for a turnaround and hadn’t looked at the broader downside risk.

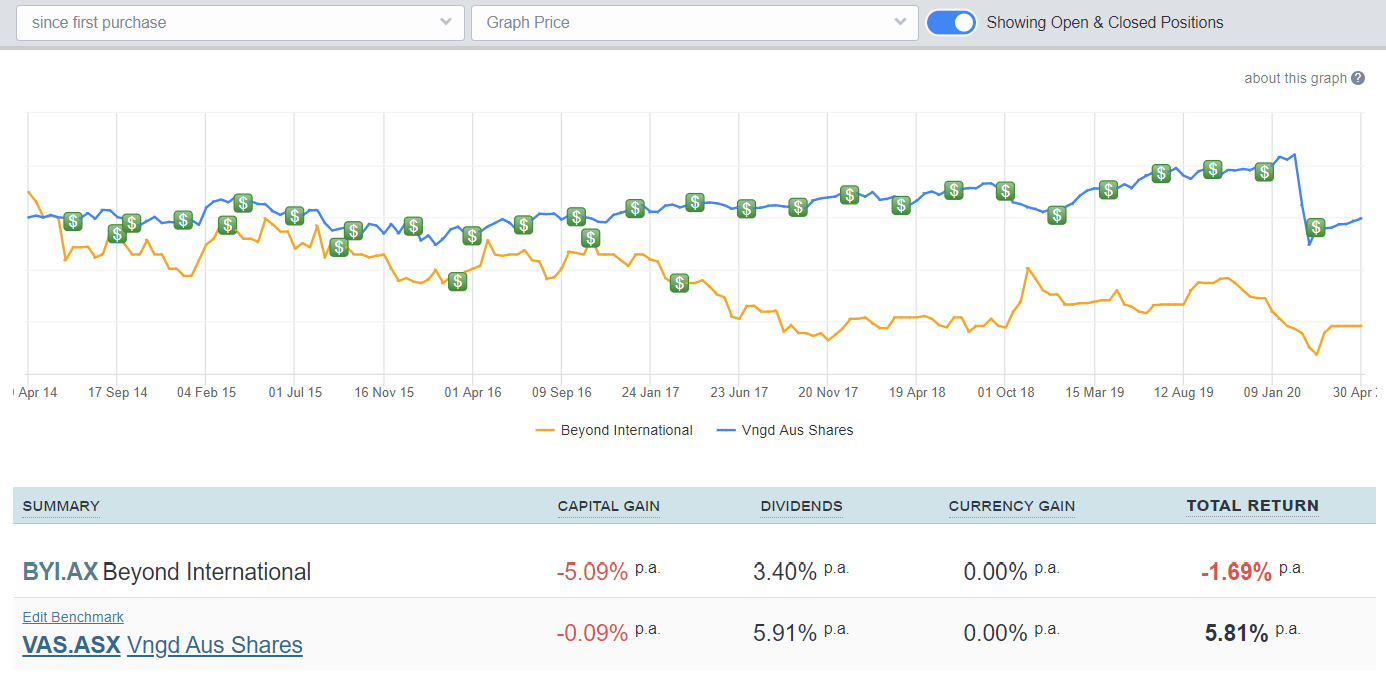

BYI stock price performance relative to the actual market.

My portfolio’s performance.

Lessons Learned:

- Just because a company is well run doesn’t mean the industry is in a good position. No matter how good your skipper is, you still rise and fall with the tide.

- Look beyond your biases, it’s easy to create a story and just see the upside. Every investment has a potential downside. Just because you can’t see it doesn’t mean it’s not there.

In summary, losses suck. But at least they make good teachers, if you’re willing to listen:

Instead of feeling frustrated or overwhelmed, I saw pain as nature’s reminder that there is something important for me to learn.

Ray Dalio

Next time on the QC: Lessons from Winners