BHS: Vista Group International – VGL:ASX

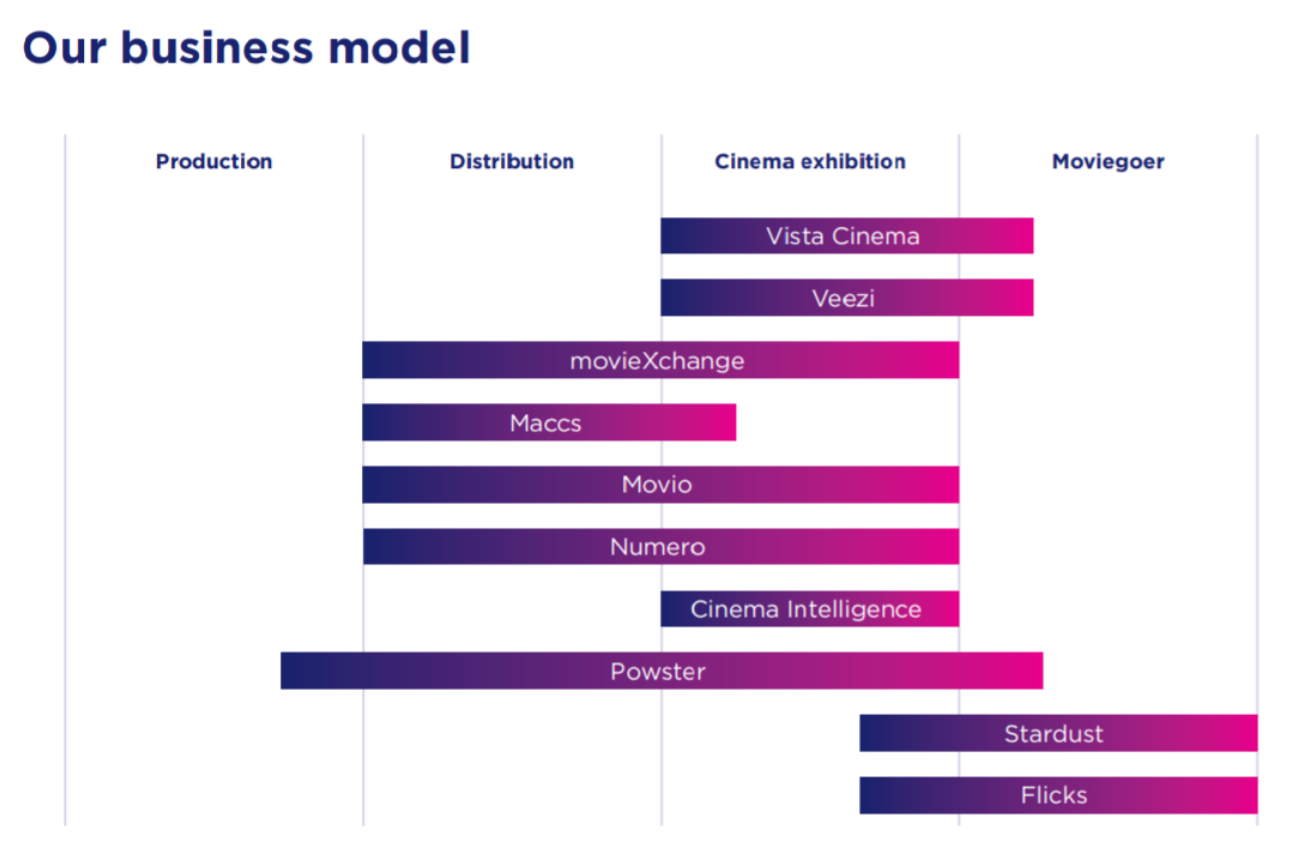

They provide a suite of software for cinemas and studios, mainly focussed on the latter end of the chain. From distribution to the moviegoer. From their site:

Additional to Cinema Management software provided by Vista Cinema, the offers of the Vista Group of companies cover moviegoer data analytics, business intelligence solutions, box office reporting software, creative and marketing services to movie studios and online movie media and exhibition information for moviegoers.

The Vista Cinema product is their biggest cash earner, accounting for about 67% of revenue. As of 2019 they have 8000 sites worldwide, 40% market penetration for the large enterprise circuit. They estimate that they add about 800 sites a year, this was lower in 2017 and may be accelerating. But should provide at least a decade of solid growth.

Movio is their second biggest earner at 18% of their revenue. In their words: “Data-driven marketing solutions for the film industry. I don’t have a complete handle on how the rest of the ecosystem works, but suffice to say, they’re collecting data from many points in the movie industry chain. This strikes me as a pretty solid competitive advantage.

Weighing Machine

RoE is lower than I would like a software company to be, hovering around the 7-8% mark. Though realistically, they are a Rev/EBITDA growth company, and these are the two metrics they mainly report on in their annuals. They pay out about 50% of their earnings in dividends, they increase their sales by about 15% per annum, with about 6% of that going to book value growth. Cash flow is maintained with a solid buffer consistently, and their debt is very manageable at ~7%. A bit worrying to me, is that NPAT is flat. I’d prefer to see more book growth under these scenarios. Dividend yield is low, sitting at around the 1% mark.

The Voting machine

Their popularity has fluctuated in the years they’ve been listed. But is generally quite high, with PE fluctuating between ~25-68x. Currently they’re on a bit of a historical low, at 27x trailing earnings. Though this is kind of to be expected given the hit to the cinema industry.

Recent events

At the end of 2019 they foresaw the COVID blow out and proactively announced that they were going to wait for a clearer understanding of what was happening before they released anymore dividends this FY.

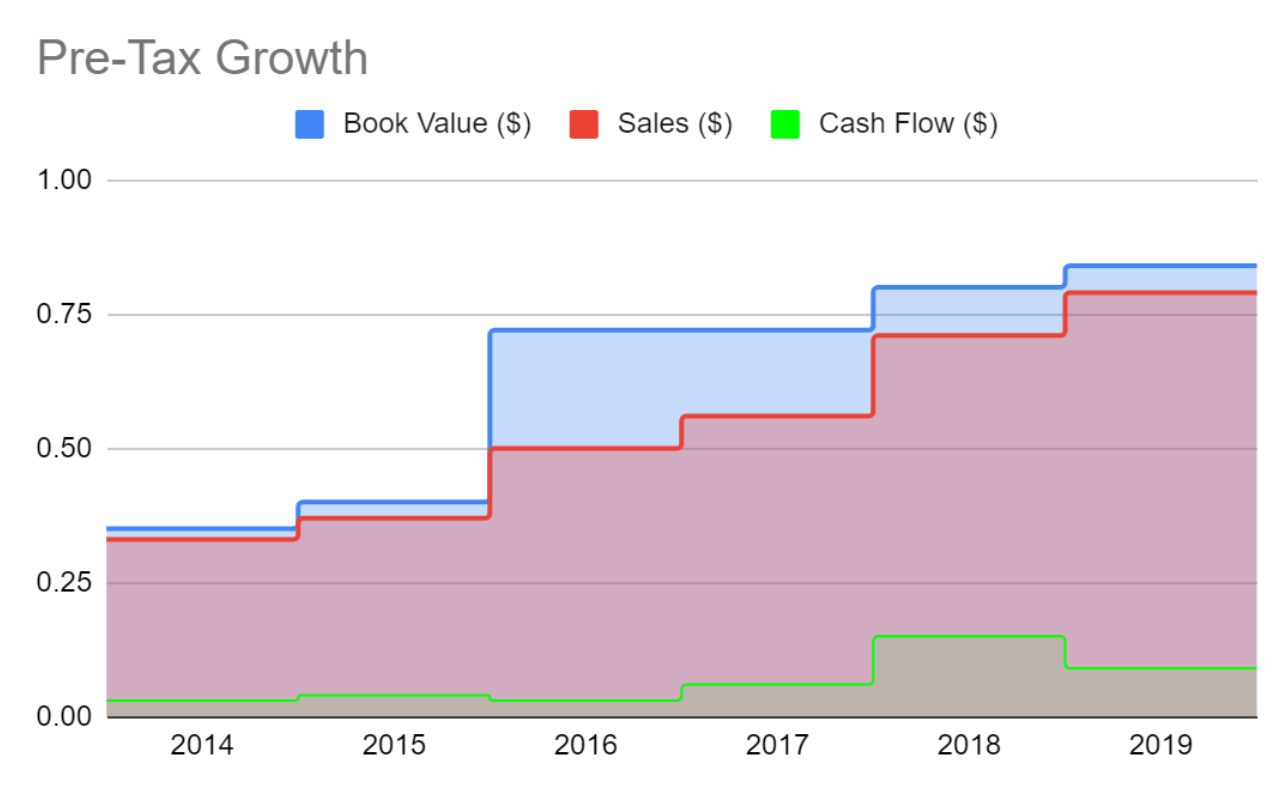

They did a bunch of capital raising when COVID hit, which is likely to permanently dilute their RoE going forward. These have been estimated and factored into the ongoing valuation. There was a heavy batch of insider buying in May at 97c. This doesn’t match the stock price at the time, the timeline matches that of the Capital Raisings. They raised NZD$116M (~AUD$108M) for 48.9M (28%) new shares. The forecast effect of this can be seen in the following graph:

They released a COVID-19 update statement at the beginning of June. They have made a number of changes to their software packages to incorporate the “new normal” from the virus. They’re undergoing a restructure of their business in order to be more nimble out the other side as they don’t know what long term changes to the industry this will bring.

80% of their clients are cinemas and heavily affected by COVID, can’t tell if they’re mission critical enough that clients will continue to pay even if cinemas are shut… Can expect a hit irrespective.

Valuation

SWSt has them valued at $0.22

My 7YCF has them at $1.44

My WeVo (With RoE heavily ballparked due to the capital raising, and EVA skewed to the BEAR model (60%) due to the unsure outlook) has them at $1.34. (This equates to about 28c of share losses to 5c of dividends over the next 3 years).

Final thoughts

Pros: I’d love to own a chunk of this business. As someone that loves movies, and the cinema, this is a really neat set of businesses to be a part of. The product end of the spectrum is fantastic, with pro-active offerings and an integrated set of products that service multiple verticals in the industry.

Cons: However, I’m not overly happy with how they’re managed. The low RoE isn’t great for a software business (industry average is 15%, the best generate 30%). Their growth rates are also not fantastic (15% sales growth, but only 6% book growth). Add the heavy pricing on top of that (popular sector, cool niche, PE of >40 usually) and there are enough cons to make them overvalued.

Result: Hold, Buy price of ~$1. Sell on a good year with a high PE expansion – $4.00