Tassal Group – TGR:ASX – EOFY20 Update

Australia’s largest vertically integrated salmon grower and seafood processor. Here are some MBI thoughts from May 2019:

- They need to expand outside of Tas to keep growing.

- Weak AUD was a tailwind.

- Salmon market growing nicely.

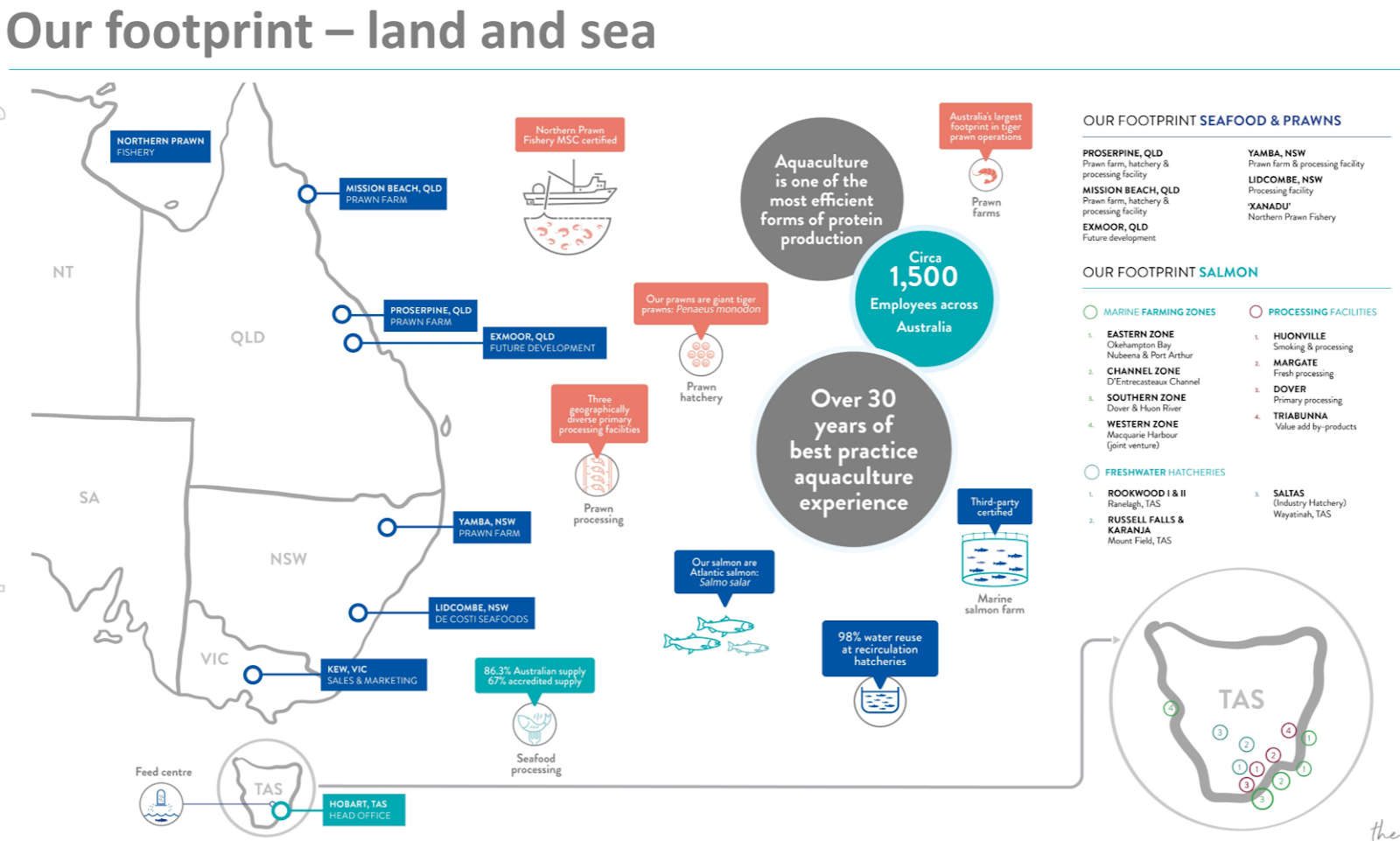

- Expanding into prawn production.

- Have a solid message of best practice and sustainability. Though they also had a breach that removed ASX certification for one of their farms.

- Some climate change risk, especially for the salmon portion of their business.

- Reasonable profit, slow organic growth. More book value growth than earnings.

- 1 Buy, 2 Holds. Buy price ranged from $3.50-$4.80

They own a number of salmon and prawn farms through Australia.

Their branding and positioning is on point for the Australian market, with a move towards quality, convenience and sustainability as some of their core tenets.

Weighing machine

They have a passable RoE usually in the high single digits, and have been consistently growing sales and book value for the last decade, though earnings haven’t kept up with these. Margin is pretty good ranging between 10-13% for the last few years. They pay out about 50% of their earnings as a dividend, and have a yield of about 5%. They dilute their sharepool a bit too much for my liking, at about 5% per annum on average, though this has largely happened in the last few years and is associated with the acquisition of the prawn farms. Debt has been at about 20% for the last few years.

Voting machine

They’re not particularly popular, trading at a PE of about 10-11x, and a PB of ~1x. Historically this has fluctuated between about 7 and 13x.

Recent events

For the last few years they have been funneling capital into growing their prawn business, as this has the potential for about 2x the EBITDA per kg of production than salmon farming (Prawn cycle is 1yr, Salmon is 3yrs). They are targeting an eventual prawn output of 20kt p.a, the FY20 forecast is 2.5kt, so there’s a good runway for growth. At today’s rates this would yield an EBITDA of about $120M (vs $15M for the prawn farm today). Expect this to grow earnings by about 5% per year.

There had been a number of headwinds in the overseas salmon market for the last few years, and Tassal had already been pivoting their business to sell more through domestic supply channels when covid-19 hit. This actually helped them, as people shifted to eating from home more and bought higher quality items. They are working to optimise their salmon production and increase it’s profitability.

There has been a lot of insider buying this year, both before and during the Coronavirus crash. Though interestingly, not much since.

As with most of the agriculture companies, there is a decent climate change/weather risk. A number of their prawn farms are in Cyclone territory, and there is some chance this is a La Nina year, which carries increased risk of cyclones and flooding in the tropical north.

Valuation

- SWSt has them valued at $4.16

- My 7YrCF has them at $6.90

- My WeVo Valuation has them at $4.96 with 17% return from dividends and 20% from Capital Gain.

Final thoughts

Pros: They are actively pursuing growth into more profitable markets through the prawn farming activity. The current Coronavirus pandemic is potentially providing them with some tailwinds as their customers’ behaviour changes. Potential system support if governments try to “bring stuff home” and protect local agriculture industries for food safety.

Cons: Earnings have been flat for a number of years, and they have been regularly diluting the sharepool to fund acquisitions etc, without actually improving their profitability. There’s some unknowns around the effect of climate change on weather patterns and their prawn farms.

Result: They are well managed, and actively working to streamline and increase profitability of the overall business. There is decent upside, and reasonable growth being driven by the prawn business. Overall the growth isn’t fantastic, somewhere between 5-9% depending on how well they implement. But they are well priced for this level of growth. Buy when the price is ~10x PE. Sell if it gets over 20x or it looks like prawn growth has capped out. Buy at $3.60. Sell at $7.20.