Quiet Contrarian. Ep 18: FY21 Reflection

Overall update – Story of the year

This was a bumper stock market year, with both the US and Australian markets hitting all time highs and posting some record gains (The All Ords was up almost 30% this year!). It’s primarily driven by record low interest rates driving up valuations, and lots of new investors/traders starting their equities journey driving up speculative prices (so many new platforms making it easier than ever to lose your money!). I personally got caught up in the furor a few times, and found myself YOLO buying (which in my experience is usually followed by YOLO selling).

I feel like this has been the first year that I’ve tried to advance beyond my initial investment strategy (Quality at a fair price) and I’ve started to dabble a bit more into cyclicals/turnarounds a bit of growth/speculation, paying more attention to the broader macro picture as well as how companies are positioned within that. It’s led to me feeling much more lost this year than I have in the past, but I’m hoping this will improve my long term investment performance as I’m better able to read and position myself through the variou market cycles. Patience has been reaffirmed as my primary weapon.

FY21 Goals and Positioning Recap

- Reduce my US holdings – In line with Long Term Debt Cycle, and the coronavirus economy hit, plus the all time TMC/GDP highs, I feel like the next few months will be a good time to reduce US holdings.

- Note: Gurufocus chose to redo all their TMC:GDP figures and calculations mid year to include the impact of the extensive QE going on.

- I transferred about 60% of my US holdings back to Australia, the US currently makes up ~16% of my portfolio. I’m happy at this level.

- Monitor the Australian market, and some of my holdings, look for opportunities to take profits if things continue to go well.

- Despite being at all time highs the AU market hasn’t gone anywhere near as crazy as the US. Happy with my current position. A few positions are quite overvalued. So I’m monitoring for opportunities to take profit.

- Gold and “defensives”? – If the economy is going to go through a period of underperformance it may be good to look at stocks that will do ok through that period. Is it acceptable to accept lower quality for less loss? Is sitting on commodities/cash a good idea?

- This has been quite the rollercoaster this year, with the allure of gold having taking a 1-2: firstly off the speculative furour in the US, and then again off the fears of Interest rates rising (where real-estate/mortgage lenders are seen as better defensive positions). I mistimed this and added to my gold holdings before the hits. Currently at ~13% holding, with solid investment theses for both companies, and I’m happy at this level.

- Re-developing my valuation and allocation method to determine how much of a stock’s returns come from dividends vs how much comes from Capital Growth. These two factors will result in different buying and selling thresholds.

- I rejigged my models, but the truth is the real success I had was finding that I like listening to Audiobooks. Have learned alot from a number of investing books, and have new ideas to rejig my models, as well as new ways to look at stocks beyond the numbers.

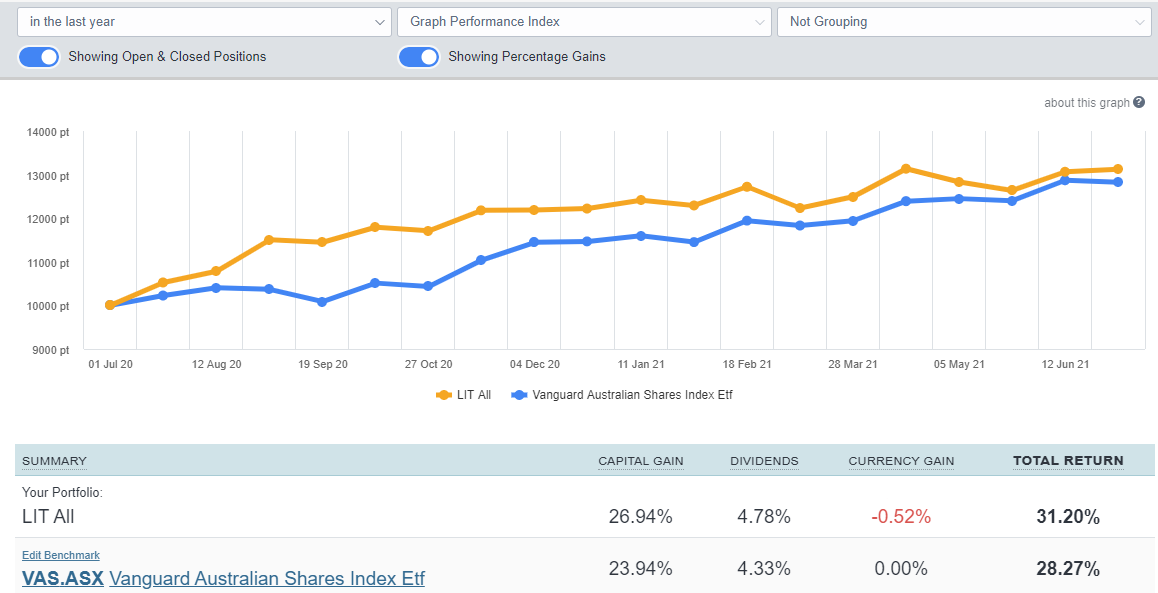

Portfolio Performance

So I beat the market this year, but only just. In the first half of the FY I managed to increase my gain over the broader market, with software and retail exposures leading the charge. The market then clawed back pretty much all of my advantage. Rotating away from my preferred sectors into mining and some of the beaten up value stocks. I ended the year with just a touch of Alpha.

| Portfolio/Index | Capital Gain | Dividends | Currency Gain | Total Return |

| LIT ALL | 26.18% | 4.78% | -0.49% | 30.47% |

| *AU | 24.65% | 4.94% | 0% | 29.59% |

| *US | 21.58% | 0.13% | -4.29% | 17.42% |

| VAS.ASX | 23.94% | 4.33% | 0% | 28.27% |

| VOO.ASX | 35.73% | 1.71% | -7.61% | 29.83% |

Best and Worst Performers

- The top 3 profitable holdings for the year were: Nick Scali, Fiducian Group, and IDP Education

- The best performers in % terms were: Pilbara Minerals, Mineral Resources, and Gale Pacific

- The worst 3 loss making holdings have been: Regis Resources, Northern Star, and Appen

- The worst performers in % terms were: Cashrewards, Retech Tech Co., and Regis Resources

You can see the power of cyclicality in both the best and worst performers: Getting it right led to huge gains in Mineral Resources and Pilbara Minerals, in which I only took small 1% positions, so total gains were minimal. But I had larger positions in Northern Star and Regis Resources, which show the dark side of timing it badly when gold fell out of favour in the second half of the year.

Finally, 2/3 of the worst performers, Cashrewards and Retech, were both speculative “punts”. I should really learn to stop punting.

Investment behaviour

Good choices

- Reading… well… audiobooks. So, listening.

- Took profit when PE ratios get too high.

- Waited more. There’s never a reason you ‘have to buy now’

Bad choices

- Got caught up in the YOLO Reddit trading mid year.

- Bought companies before I had my understanding and story worked out properly.

- Sat on too much undeployed cash.

FY22 Goals and Positioning

Goals

- Improve portfolio management. The aim is to move towards being regularly fully invested, rotating the portfolio into and out of sectors/holdings as they become over/undervalued.

- Analyse more companies and improve my circle of competence.

- Try to understand trading strategies a bit more. May devote a small part of my holdings to running a trading portfolio.

Positioning

Market is looking toppy, much like it did in FY19, though this time there’s only been a 1 year run, as opposed to the 10 year run leading to FY19. The broad macro environment we seem to be functioning in:

- QE – MMT and the free money in the system, the last time we did this there was a 10 year bull run.

- This will lead into the De-carbonisation economy and massive infrastructure spend – which is a long term play

- Low interest rate environment until ~FY23, will inflate equity prices for a little while. Pay more attention to valuations in light of a potential correction.

- Trade war with China.

- Deglobalisation and inflation.

- Shift in demand from Goods to Services – I think alot of the goods purchases that did so well in FY21 will not be repeated in FY22. Expect EPS pullback from some of the best performers.

- Pent up demand for travel – Expect a bumper year for tourism as things open up. The aim for this is before actual numbers come in.

The problem with alot of the more obvious ways to play these trends is that they’re well known, so the companies are overpriced. Oh well. No such thing as a free lunch.